Gestalten Sie personalisierte Finanzerlebnisse für Ihre Kunden mit den Produkten, Lizenzen und Tools von Yapily.

Payment-Produkte

Daten-Produkte

Tools & Services

Entdecken Sie vielfältige Use Cases und sehen Sie, welche Innovationen Kunden aus verschiedenen Branchen mit Open Banking realisieren.

Holen Sie das Beste aus der Yapily-API heraus – mit einer erstklassigen Dokumentation und einer einzigen Schnittstelle zur Verwaltung der Integrationen.

Für Entwickler

Erfahren Sie mehr über unsere Mission und die kreativen, engagierten und innovativen Köpfe, die uns dabei helfen, sie zu erfüllen

Unternehmen

Eine neue Art, Zahlungen zu leisten

Überweisen Sie Geld im Handumdrehen von einem Konto zum anderen. Keine Vermittler:innen, keine versteckten Gebühren, grenzenlose Möglichkeiten.

>2000

Banken und Finanzinstitute sind bereits in unsere Plattform integriert

19

Länder mit mehr als 95 % Kontodeckung in jeder Region – Tendenz steigend

>3500

Anwendungen, die von Kunden erstellt wurden und von Yapilys API unterstützt werden

Entscheiden Sie sich für Komfort

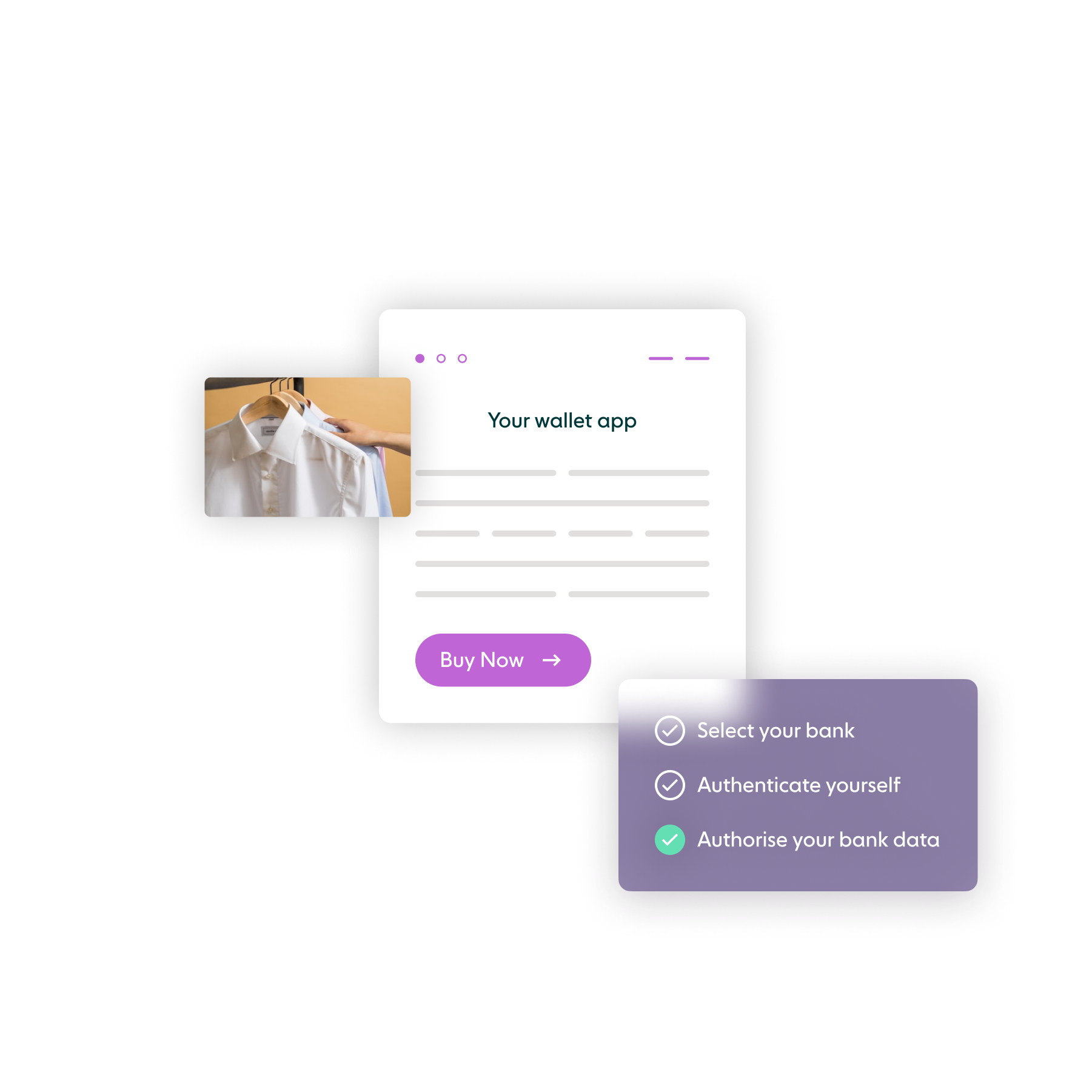

Ermöglichen Sie sicher und einfach direkte Konto-zu-Konto-Zahlungen aus jeder Anwendung heraus

Automatisieren Sie die Dateneingabe

Bieten Sie ein automatisches Ausfüllen der Zahlungsdaten, um die Eingabe zu beschleunigen und Eingabefehler zu vermeiden

Sicherheit hat Priorität

Verringern Sie das Betrugsrisiko bei Zahlungen von und schützen Sie Kundendaten mittels starker Kundenauthentifizierung (Strong Customer Authentication, SCA)

Beschleunigen Sie die Zahlungsabwicklung

Senden und empfangen Sie Geld von Bank zu Bank schneller mit Faster Payments in UK und anderen lokalen Zahlungssystemen

Reduzieren Sie Kosten

Kartensysteme, Interbankenentgelte (Interchange Gebühren) und unnötige Vermittler:innen gehören der Vergangenheit an

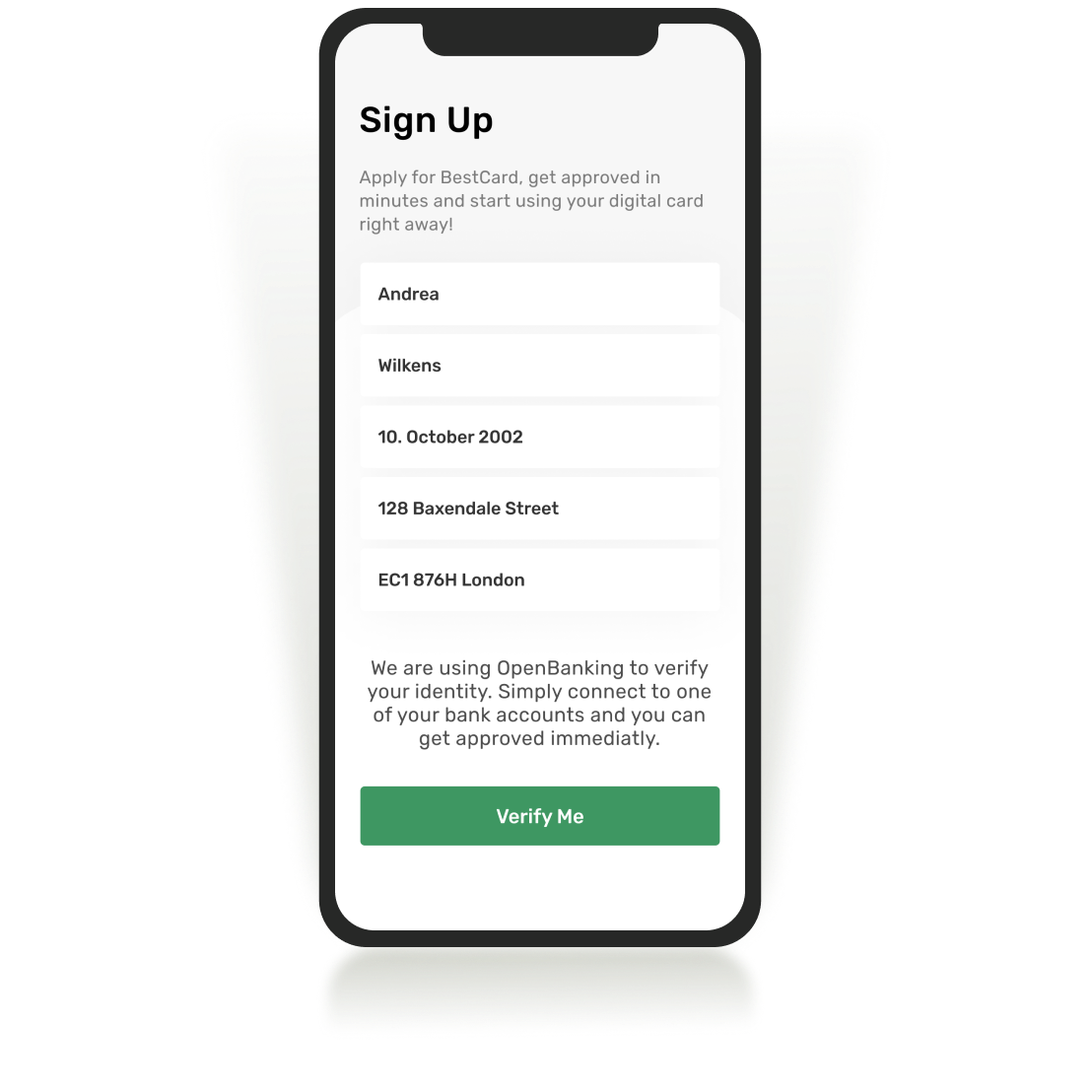

Schützen Sie Ihre Kund:innen

Es werden keine Karten- oder Bankdaten weitergegeben oder gespeichert – für ein geringeres Betrugsrisiko

VON ENTWICKLER:INNEN FÜR ENTWICKLER:INNEN

Überlassen Sie uns die zeitraubende Arbeit

Unsere API steuert Ihre Anwendungen im Hintergrund, damit Sie sich voll und ganz auf Ihr Produkt konzentrieren können.

Einfachheit ist das A und O

Schneller und einfacher Start mit erstklassiger Entwicklerdokumentation und jederzeit verfügbarem Support.

Lizenz? Darum kümmern wir uns

Bringen Sie sichere Innovationen im Zahlungs- und Datenbereich auf den Weg, ohne zusätzliche Lizenzen einholen zu müssen.

Mit Open Banking eröffnen sich Ihnen ungeahnte Möglichkeiten