Amidst a competitive payment environment with multiple intermediaries and touchpoints, Pay by Bank emerged from the open banking framework to allow for more direct and simple account-to-account transactions. It’s a secure and convenient method that can help improve experience for the user with real-time payments, and increase conversion rates for the business.

So let’s uncover more about what Pay by Bank is, and how you can seamlessly integrate it into your business operations for maximum efficiency.

What is Pay by Bank?

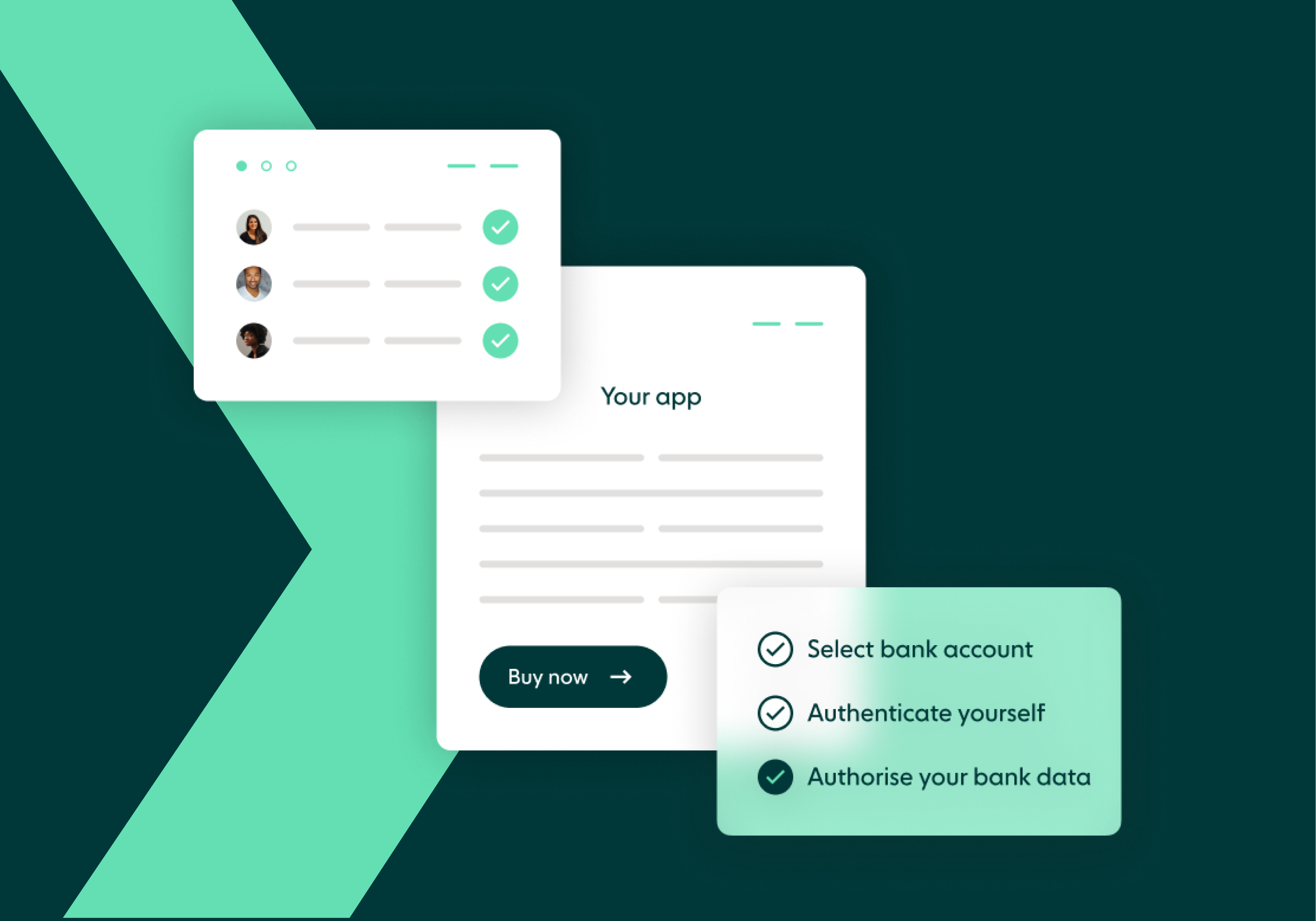

Pay by bank leverages existing payment rails but is powered by open banking to enable faster and more secure transactions. Customers use biometrics like their fingerprint or Face ID to approve the payment via their bank’s online platform or app. Pay by Bank includes Account-to-Account (A2A) payments, where money is directly transferred from one bank account to another.

Explore this secure way to pay that can save your business time and money.

Benefits of Pay by Bank

There are numerous benefits which make Pay by Bank a popular choice amongst merchants and consumers:

- Reduced merchant costs: Pay by Bank cuts operational expenses for merchants by eliminating chargebacks and reducing the fees associated with traditional card transactions, leading to more cost-effective payment processing.

- Rapid funds settlement: This system ensures that payments are processed swiftly, with funds typically landing in the merchant’s account almost instantly, thanks to integration with the Faster Payments Scheme, thereby improving cash flow.

- Superior security: By utilising multi-factor authentication through customers’ online banking, Pay by Bank significantly lowers the risk of fraud and minimises manual errors, offering enhanced security for both parties involved in the transaction.

- Extensive coverage: Given that a significant portion of the UK and European populations have bank accounts (99.76% in the UK as of 2021), Pay by Bank is an accessible and preferred payment method for a wide range of customers.

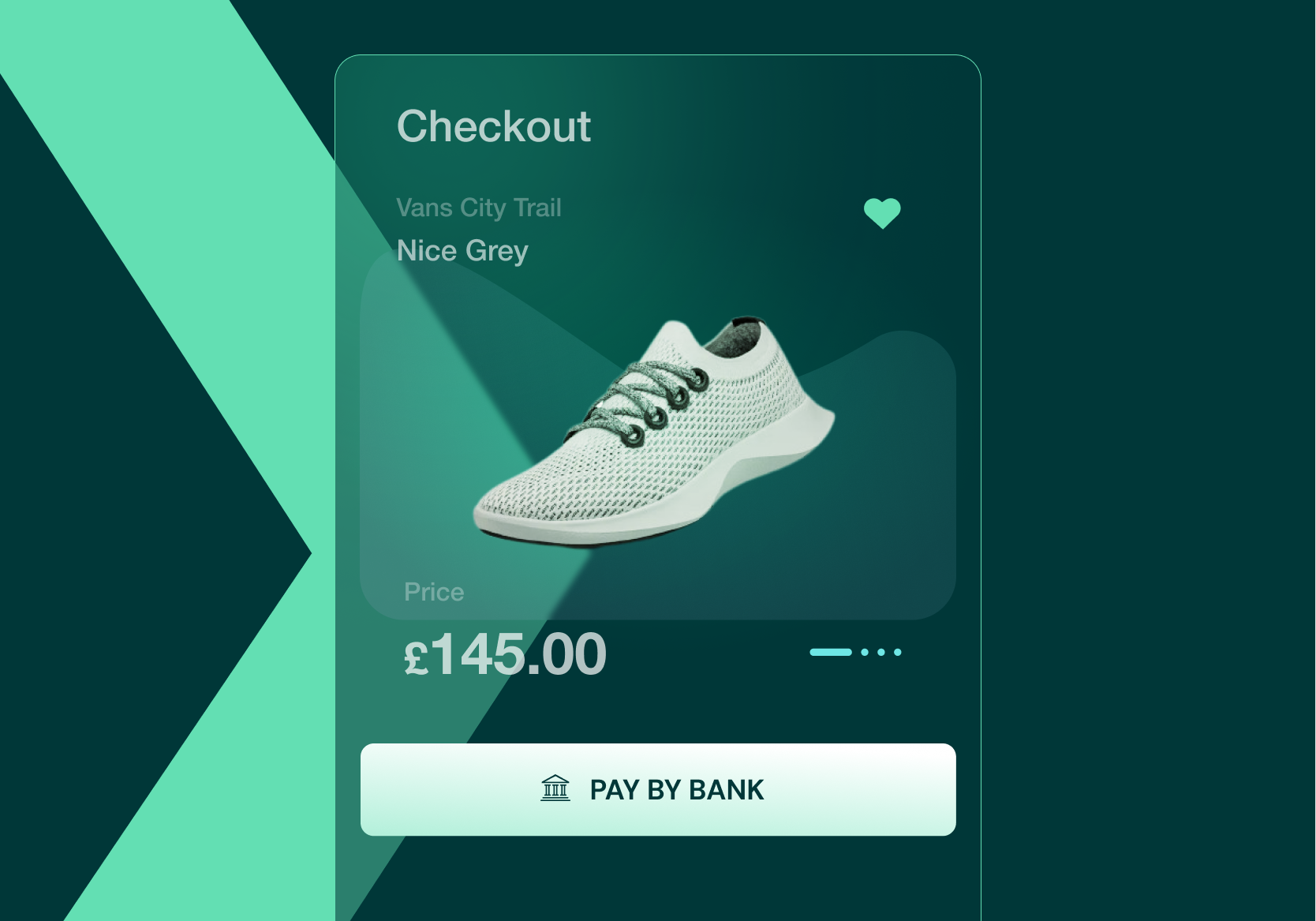

- Seamless experience: The payment process is streamlined to just a few clicks, allowing customers to complete transactions easily without the need to input extensive banking details, thereby offering a more convenient and user-friendly checkout experience.

Pay by Bank is proving popular amongst some of the Big Tech players to get the additional competitive edge and escape legacy costs or delays to settlement.

Challenges of Pay by Bank

Ensuring more businesses and consumers get on the bandwagon of using Pay by Bank comes with a set of challenges. On paper, it offers advantages to speed and security that are two core elements when making a payment.

It seems that adoption of the Pay by Bank method would rise if there was greater education in place that would elevate trust in this way to pay. Consumers may still gravitate towards digital wallet methods like Apple Pay or Google Pay, which offer simplicity but not the same benefits that Pay by Bank provides.

In some cases, the prevention of wider adoption of Pay by Bank can simply be the situational result of the region or business not offering it as an option. Once these regions improve their national payment rails, it can strengthen the security and speed of payments by offering Pay by Bank.

Is Pay by Bank safe?

There are robust measures in place in order for businesses and their customers to feel safe and secure using Pay by Bank. PSD2 ensures Strong Customer Authentication (SCA) in place so multiple checks are in place to confirm the consumer’s identity in order to make the payment.

Rather than customers’ details being stored by the business, once a customer initiates Pay by Bank, they are redirected to their bank’s mobile app. In order to approve the payment, the customer uses biometrics such as Face ID or their fingerprint to consent to the payment going forward. This also helps prevent fraud with the additional layer of security enabled to ensure only the legitimate account holder makes the payment.

As Pay by Bank adheres to the UK and Europe’s data protection and privacy laws, such as GDPR, as well regulatory requirements, it benefits the business and the consumer. Businesses can have peace of mind they are compliant and consumers can be sure their data is being handled responsibly.

European coverage of Pay by Bank

As we’ve discussed, the Faster Payments Scheme in the UK has ensured Pay by Bank can be adopted with ease, and allows businesses to offer this to their customers with peace of mind. In October 2022, the European Commission adopted legislation to make instant payments in Euro secure, instant, and cost-effective. This helps to remove the barriers to integrating open banking for businesses. We’re seeing greater open banking adoption maturity with Germany, France, and the Nordics who have invested in improving payment experience.

When PSD3 comes into effect, this will offer further support for user protection and improve access to payment systems. Another key focus will be on PISPs and banks strengthening their anti-fraud measures including SCA and reducing false positives. The combination of these elements will help businesses optimise conversions with open banking.

Mairead McGuinness, Commissioner for Financial Services, Financial Stability and Capital Markets Union commented on this, “Today we are proposing a set of measures including enhanced protection for consumers making electronic payments in the EU and improved criteria to prevent and remedy payment fraud. This proposal will ensure customers and businesses benefit from more innovative payment and financial service options, whilst being confident that these are offered in a safe, transparent and secure way.”

What is the future of Pay by Bank adoption?

While open banking has seen accelerated adoption across the UK and into Europe, as well as increased hype penetrating US markets, there has been an initial pause by some to adopt pay by bank. Looking further afield, South Korea, Australia and India have developed their open banking systems which have gained traction, whilst Canada, Hong Kong, Japan, and further parts of Asia are preparing for open banking.

As open banking relies on existing payment rails, markets where there are existing issues will not be completely bypassed by using pay by bank. However, with clear efforts being taken into addressing these issues, the impending PSD3 proposal, and the JROC’s December report which displayed a roadmap of 29 actions across 3 phases in the next 2 and a half years.

Pay by Bank provides speed, security, and an enhanced experience to both businesses and their customers so is sure to gain further traction as we garner education and trust. We are seeing further proof points of reduced fees and improved experience from businesses using open banking across various sectors, and with these results comes increased adoption.

Ready to get started with Pay by Bank?

If you are ready to reap the benefits that Pay by Bank can offer for your business and your customers, speak with one of our open banking experts. Your business can provide a seamless payment experience that is more cost-effective and secure so you can focus on growing your business globally.

Discover how Pay by Bank can transform your payment process!