Imagine a future where consumers no longer need to search, scroll, or click “buy” for every item they need. Instead, they simply enter a prompt outlining their needs, whether it’s restocking their cupboards or securing the best flight to Berlin next week. An intelligent assistant then handles the entire purchasing journey autonomously.

This is agentic commerce, and it will rewrite e-commerce.

It means merchants will no longer only market products and services to people; they will need to market to algorithms. For Payment Service Providers (PSPs), it means adapting their services to operate in the complex machine-to-machine economy, raising challenges around payment authentication, security, and the use of consumer spending data to feed the agents. Top PSPs like Checkout.com, Worldpay, and Adyen are already putting agentic commerce front and centre.

To maintain market share, PSPs must keep up with this market evolution. This means learning the fundamentals of agentic commerce so you’re ready to enable merchants with this new technology when the shift happens.

What exactly is agentic commerce?

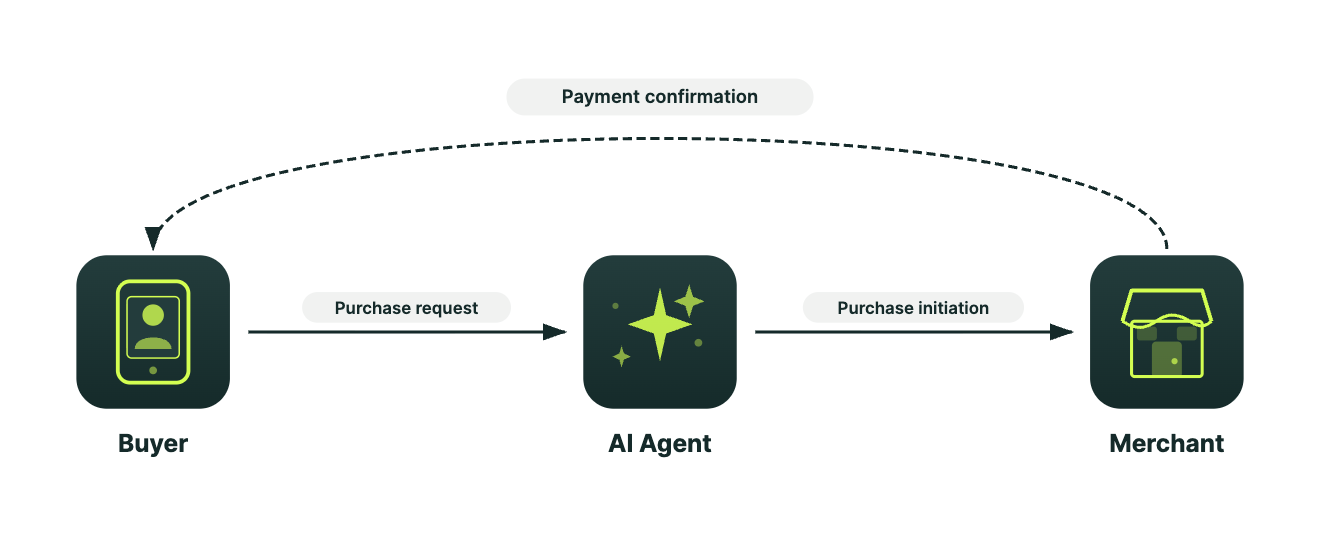

At its core, agentic commerce uses AI agents to buy goods autonomously on behalf of shoppers, operating strictly within predefined parameters set by the user.

This provides an alternative way for people to search for and buy goods that removes friction entirely. It has the power to offer a “personalised” shopping experience across the online shopping spectrum, from personalising search for high-end goods, to automating the purchase of day-to-day household products. It will provide another powerful, automated channel that merchants can offer to meet specific purchasing behaviours.

Discover how agentic commerce can form part of your wider open banking growth strategy in our article: Beyond the checkout.

Discover how agentic commerce can form part of your wider open banking growth strategy in our article: Beyond the checkout.

Bridging the infrastructure gap with open banking payments and data

Agentic commerce is currently in its building phase. Projects from the world’s biggest payments and tech companies, like Google's Agent Payments Protocol (AP2) and Mastercard's agentic commerce protocol, and Coinbase’s x402 protocol, prove its momentum.

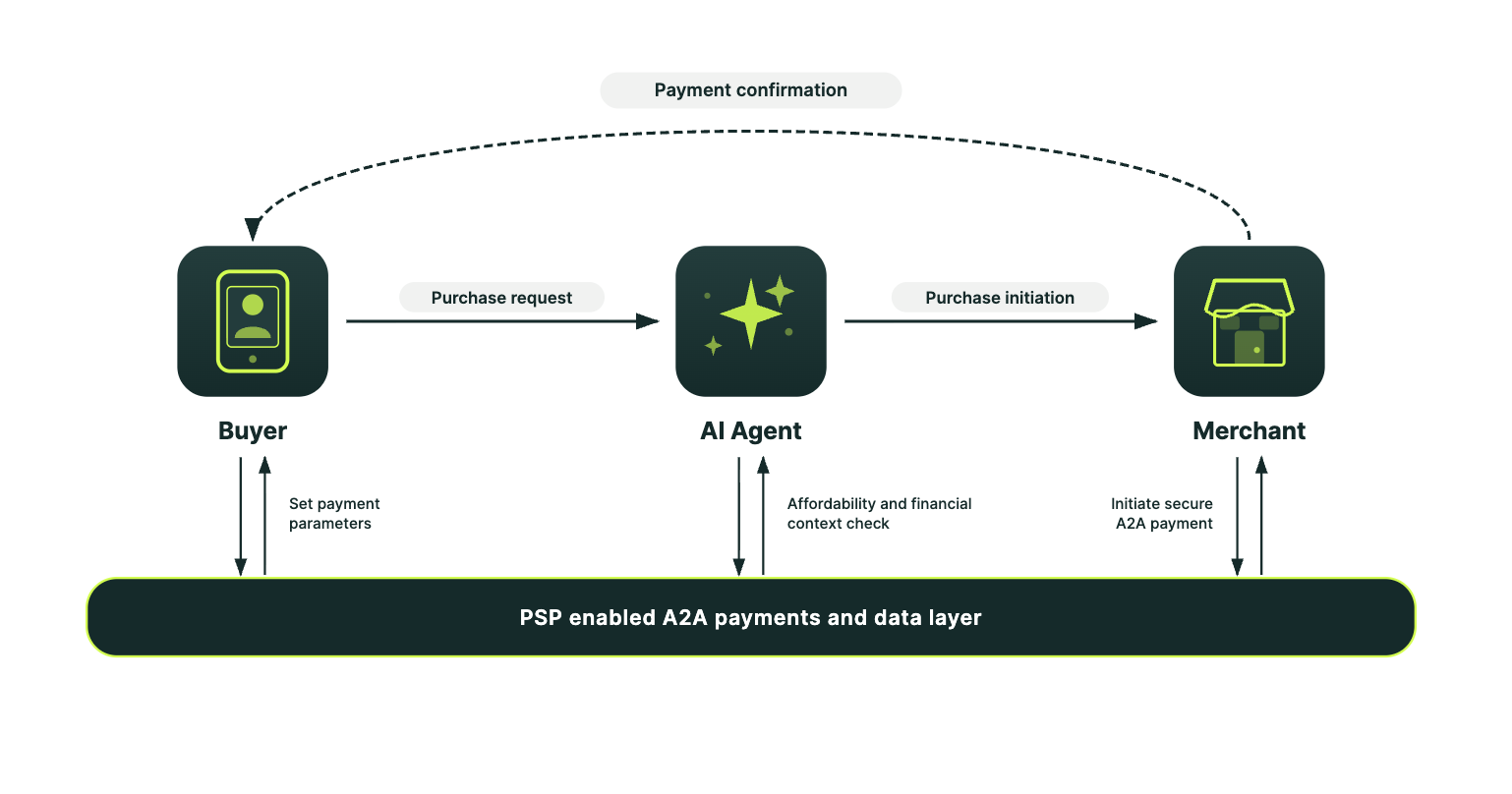

But what connects these high-level protocols to a person's actual financial data, and how do you initiate payments with real-time precision while remaining secure and in control? The answer is infrastructure that provides secure execution alongside real-time management capabilities.

Open banking payments (PIS) and cVRP: Open banking provides an authorisation mechanism to manage AI agents’ authority to make payments. And, with the introduction of Commercial Variable Recurring Payments (cVRP), which allows prolonged authorisation for payments to be taken only within strict, predefined parameters and limits, users won’t need to authorise each purchase. This process is vastly more controllable than Direct Debit.

Open banking data (AIS) setting the stage: AIS provides the real-time, comprehensive account visibility an AI agent needs to understand a user's financial context and build a safe profile of affordability long before a transaction occurs. The focus is on creating safe, frictionless payment rails that are fundamentally machine-friendly.

Learn how combining open banking payments and data comes together to compound growth in our recent article: Open banking’s compounding advantage.

Learn how combining open banking payments and data comes together to compound growth in our recent article: Open banking’s compounding advantage.

To illustrate how this works in practice, here is a step-by-step breakdown of a typical agentic commerce transaction:

The buyer initiates: A buyer tells their AI agent, "Book me a direct flight to Berlin for next Friday, returning Sunday, keeping the total under £200."

The AI agent checks affordability (AIS): Before searching, the AI agent uses open banking data to securely view the buyer's real-time bank balance and transaction history. It confirms whether the £200 limit is well within the buyer's current affordability and spending parameters.

The AI agent researches merchants: The AI agent scans airline APIs (the merchants), comparing flight times, baggage policies, and prices to find the exact flight that meets the buyer's criteria.

The AI agent initiates payment (PIS): Once the ideal flight is secured, the AI agent uses cVRP to instantly initiate a secure, account-to-account transfer. The payment is authenticated in the background without the buyer needing to dig out a credit card or manually pass 3D Secure checks.

The merchant fulfills the order: The merchant receives instant settlement and issues the ticket. The buyer receives a simple notification: "Your flight to Berlin is booked and paid for." either through the LLM directly, or as a confirmation email from the merchant (or both).

The reality and risks of agentic commerce

Agentic commerce is projected to move $3 trillion to $5 trillion of global revenue for the online retail market by 2030. But, as the OpenClaw “ClawHavoc” hijackings prove, there are risks that need to be overcome before merchants will confidently trust agentic commerce at scale. Understanding exactly what this shift means for your business, your tech stack, and your payment architecture right now will mean you’re structurally ready when it becomes a reality.

On the consumer side, research from Bain highlights that only 24% of consumers are comfortable using it to make a purchase. WorldPay’s (Worldpay Agentic Commerce Report 2025) shows their top worries include:

Identity theft (55%)

Incorrect purchases (55%)

Unauthorised purchases (54%)

Fraud (53%)

Losing financial control (51%)

For the multi-trillion-dollar potential to be realised, the industry needs infrastructure that inherently addresses these fears. Consumers will not delegate spending power until they feel protected, informed, and in control.

Solving the trust equation

WorldPay’s research shows that consumers want fraud protection (54%), the ability to cancel within 24 hours (50%), the ability to review before purchase (49%), real-time alerts (42%), and clear spending limits (41%).

Open banking directly answers these trust builders:

Consumer demand | Open banking solution | How open banking solves it |

Fraud protection | Secure Customer Authentication (SCA) & API encryption | Pre-authenticates automated payments when setting parameters, drastically reducing the risk of unauthorised purchases. |

Ability to cancel within 24 hours | cVRP | Users maintain absolute control and can instantly revoke an AI agent's payment access or cancel future automated payments at any time. |

Ability to review before purchase | SCA and AIS | Gives the AI agent real-time visibility into finances, so users can choose to review and authenticate payments for proposed purchases. |

Real-time alerts | Instant settlement | Direct account-to-account transfers triggers immediate, real-time notifications the second an agent initiates a payment. |

Clear spending limits | cVRP | Allows users to set strict, predefined boundaries (like maximum transaction amounts or total monthly limits) that the AI physically cannot exceed. |

As open banking adoption grows across Europe, consumer trust and familiarity will naturally increase. As consumers become more accustomed to using open banking, their trust and familiarity in its processes and interface will increase, helping mitigate any distrust of agentic payments.

Making future-readiness your competitive edge

In an increasingly competitive payment processing industry, PSPs need every opportunity at their disposal to future-proof their competitive edge.

Preparing for agentic commerce allows PSPs to:

Win merchants pioneering agentic commerce: Move away from competing purely on transaction fees to attract forward-thinking merchants and those specifically positioned to serve agentic shopping experiences.

Prepare for an immediate shift in e-commerce payments: Agentic commerce is already here and accelerating quickly. Agents will be making regular payments sooner than you think, and if you are not ready in time, you could be stuck playing catch-up, potentially losing merchant accounts in the process.

Position yourself as a strategic partner: Show merchants that you can guide them through complex technological shifts.

PSPs that integrate open banking payments and data now will be much better positioned from a technical perspective when agentic commerce scales.

The winners in the agentic commerce era will be the ones consumers trust to protect their data. Open banking combines financial data access and bank-to-bank payment initiation, creating the infrastructure required for secure agentic transactions.

Are you using open banking to strengthen your agentic commerce strategy? Speak with one of our open banking experts today to discuss how integrating open banking payments and data can support your agentic commerce development.