Yapily recently hosted a panel discussion on how intelligent data and integrated payments are impacting lending, bringing together leaders from across the market to look at what is working today and where the industry is heading. The conversation was chaired by Jason O'Shaughnessy, Director of Lending at Yapily, and joined by Tigana Sari, Product Owner at Allica Bank, Kai Hunter, COO and Chair at Lovey, and Kate Kennedy, COO at Navrisk. Over the hour, the group worked through four connected themes:

The state of underwriting today, and what slows teams down.

Turning raw bank data into reliable signals.

The role of AI in credit decisions.

Open banking beyond the point of origination.

This article pulls out the main threads from each, along with the live audience polls that captured where the room stood.

Watch the full webinar recording here.

Watch the full webinar recording here.

The state of underwriting today

The panel opened on a point that reframes how many teams think about speed: the slow part of lending is rarely the decision itself. Most of the effort, and most of the delay, goes into everything that comes before it: gathering documents from scattered sources, manually reviewing financial statements, and reconciling inputs that arrive in different shapes and standards. There’s huge administrative effort needed before an underwriter can simply start assessing a case.

That framing matters because it changes what "faster" should mean. Speeding up a decision that rests on thin or poorly prepared information helps no one, and several speakers were wary of chasing speed as a key indicator of performance. The stronger opportunity, the group suggested, is in giving underwriters better and cleaner information to work with, so that the judgement they apply rests on something solid.

"For me, it's not about the speed of the decision, it's about the correctness of the decision."

Kate Kennedy, COO, Navrisk

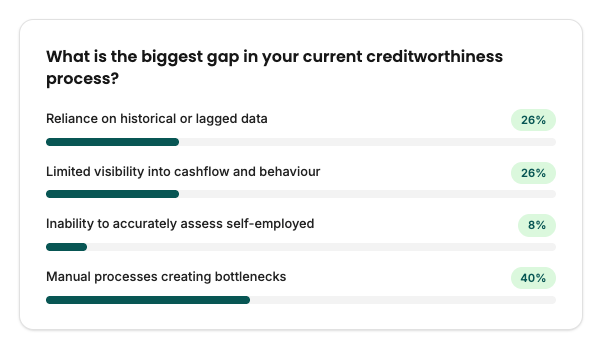

The audience saw it much the same way. Asked where the biggest gap in their creditworthiness process sits, the largest group, at 40%, pointed to manual processes creating bottlenecks, ahead of lagging data and limited cashflow visibility. The friction most teams feel, in other words, is in the manual nature that typically comes with preparing a case, which is exactly the upstream work the panel had been describing.

From raw bank data to reliable signal

If the first theme was about the work before a decision, the second narrowed in on the raw material itself. With open banking now part of everyday life for a growing share of borrowers, the panel agreed that access to data is largely a solved problem. What comes off a bank feed, though, is rarely ready to use. It tends to arrive messy and inconsistent; it varies from one provider to the next, with many still requiring manual uploads to verify data, perform fraud checks, and it needs real work before a model or an underwriter can use it with any confidence.

This is why the conversation kept returning to enrichment and categorisation, and to a distinction the group felt was easy to miss. What counts is whether the data is genuinely useful and sharpens a specific decision, because more data on its own simply adds noise and cost. Contributors described the goal as reaching a point where skilled people spend their time interpreting what an account is telling them, instead of first wrangling the data into a usable state.

"You can't get more granular than what flows through bank accounts."

Kate Kennedy, COO, Navrisk

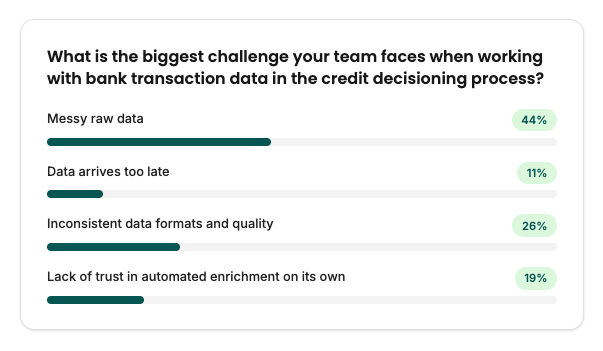

The poll pointed the same way. Asked about their biggest challenge working with bank transaction data, 44% chose messy raw data, and another 26% chose inconsistent formats and quality, so around seven in ten located the problem in the state of the data itself rather than how quickly it arrives. On that evidence, the bottleneck has moved from getting hold of information to being able to trust it.

AI in credit decisioning

The third theme turned to AI, which several panellists described as moving from experiment to everyday tool. The framing that held the discussion together was that AI is most useful as support across the lending lifecycle, taking on the clear-cut work so that people can concentrate where judgement is genuinely needed. Where the data is complete and clean, an automated decision can be quick and easy to stand behind. The harder task, the group agreed, is with businesses with complex financial history that cannot be categorised in the same way as simple businesses, leading to manual review still needing to be done.

A recurring argument was that a "yes" is usually straightforward to evidence, while a "no" often is not, and that this asymmetry carries real consequences for borrowers who might reasonably have been served. It led the group to a few shared principles:

Accountability for a decision should stay with people, whatever part automation plays in reaching it.

Governance and explainability should be treated as non-negotiable.

Declines, in particular, deserve a human check before they become an absolute no.

"You want those nos, before they become an absolute decline, to go to a human sanity check."

Kai Hunter, COO and Chair, Lovey

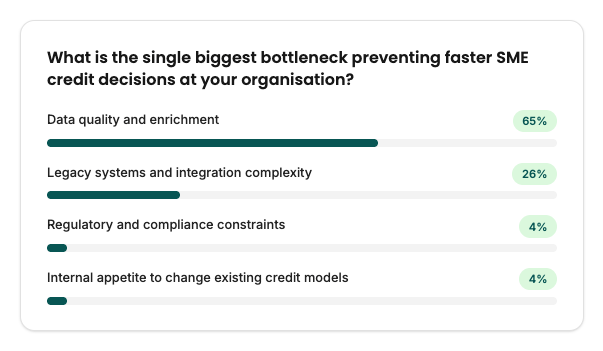

Where the audience placed the real constraint says a lot. Asked for the single biggest bottleneck to faster SME credit decisions, 65% chose data quality and enrichment, well ahead of legacy systems at 26%, with regulation and internal appetite barely registering. Even in a discussion about AI, the room kept coming back to the data feeding it, mirroring the earlier point that better inputs, more than faster models, are what move decisions forward.

Open banking beyond the point of origination

The final theme looked past the moment of approval. A recurring idea was that a loan is a relationship over time, and that the same open banking connection used to make the original decision can keep working long after it. Continuous visibility can help a lender notice when an account is drifting from healthy towards stressed, opening the door to a constructive conversation earlier and potentially well before a problem becomes a default.

Several speakers were more ambitious, describing a shift from reacting to anticipating. With a live view of how a business is actually trading, a lender can begin to see needs forming and reach out before the customer has to ask, which moves the relationship closer to a genuine partner than a provider waiting to be approached.

"Can we make a world where we can proactively, as lenders, come to you when we know you're going to need finance?"

Tigana Sari, Product Owner, Allica Bank

Payments are where much of this becomes concrete, which is what the final poll explored. Asked which payment capability would add the most value to their lending proposition, the largest share chose loans that settle instantly after a decision, while the rest of the votes gathered around more resilient repayments. Both pull in the same direction: moving money in and out dependably is becoming as much a part of the proposition as the credit decision itself.

Payments are where much of this becomes concrete, which is what the final poll explored. Asked which payment capability would add the most value to their lending proposition, the largest share chose loans that settle instantly after a decision, while the rest of the votes gathered around more resilient repayments. Both pull in the same direction: moving money in and out dependably is becoming as much a part of the proposition as the credit decision itself.

The thread running through it all

For all the ground the panel covered, one idea connected every theme: the data lenders need is largely already there, and the real opportunity is in what they do with it. Across the session, speakers kept returning to the same combination: interpreting information well, acting on it earlier, and keeping people in the loop as automation takes on more of the routine work. That, more than any single tool, is what the panel saw shaping the next phase of lending.

The full recording goes into far more detail, including practical examples from the panel.