In this blog, we celebrate another type of technology. It is less well-known but is having a similarly game-changing effect on our relationship with financial services.

The crucial role of APIs

Following the implementation of open banking regulations by the European Union in 2018, API (Application Programming Interface) technology immediately became an essential enabler for a new generation of financial services.

With the account holders’ permission, APIs enable the passing of account data from the more traditional banks to the financial service providers so they can deliver ground-breaking services for both consumers and business customers. While no actual payments flow through the APIs, the customer data gives third-party insights into the customers’ financial situation and spending habits.

Initially, APIs were unpopular with legacy banks which had change forced upon them. They had to spend time and money on building APIs, and the change made access to customer data more widely available to more service providers. This has seen many new entrants into the space, increasing competition and allowing for better, fairer financial services.

1 Opening the doors to more competitive financial products

APIs have enabled a wave of innovation in financial services. Before open banking and APIs, financial services were a bit like watching TV in black and white. API technology brought vivid colour, innovation and closer relationships with consumers.

Since its launch, the adoption of open banking services by both consumers and businesses continued its rapid growth. In July 2023, a new high of 11.5m open banking payments were made reflecting an increase of 9.3% over the prior month. Comparing year-to-date (YTD) data for 2023 to 2022, total open banking payments have grown over 102%.

APIs are the secret sauce enabling easy access to data and A2A payments so new fintech service providers can tailor their offering much more closely to customer needs and circumstances.

2 Why we need an alternative to card payments

For many years, if a business wanted to accept payments in anything other than cash, they had to go down the route of Visa and Mastercard, which have always significantly increased the costs of doing business.

The average costs of traditional payment acceptance are between 1.5% and 3.5% plus transaction fees that are often between 1 and 3% of the sale value. Open banking transactions are just a fraction of this cost with a fixed fee per transaction that can be as low as 0.19%. with no other third-party charges.

3 Enabling greater financial responsibility and inclusion

The changes and advances enabled by API technology have been huge, and enable faster access to data.

The data that is available via APIs now give open banking service providers far deeper insights into the customers’ individual circumstances such as the ability to take into account fluctuating income from the roles in the ‘gig economy’. This data means they can accurately assess affordability and creditworthiness to help customers avoid defaults and maintain financial stability.

4 A more seamless customer experience

Open banking and API technology have enabled a leap forward in customer experience and convenience. Single-use mobile payment methods such as paying by a link or QR codes are now part of the open banking experience. For the customer, these offer a way to pay with little effort and zero risk of human errors. There is also no need to share personal bank account information so less risk when requesting a payment.

Consumers no longer accept clunky processes for online checkout, and unnecessary friction often meaning lost sales. Forbes reports that on mobile devices alone, the cart abandonment rate is 84%. By reducing the number of parties involved in payment transactions, simplifying re-directions and increasing transaction speed, businesses can help prevent cart abandonment and reclaim previously lost transactions.

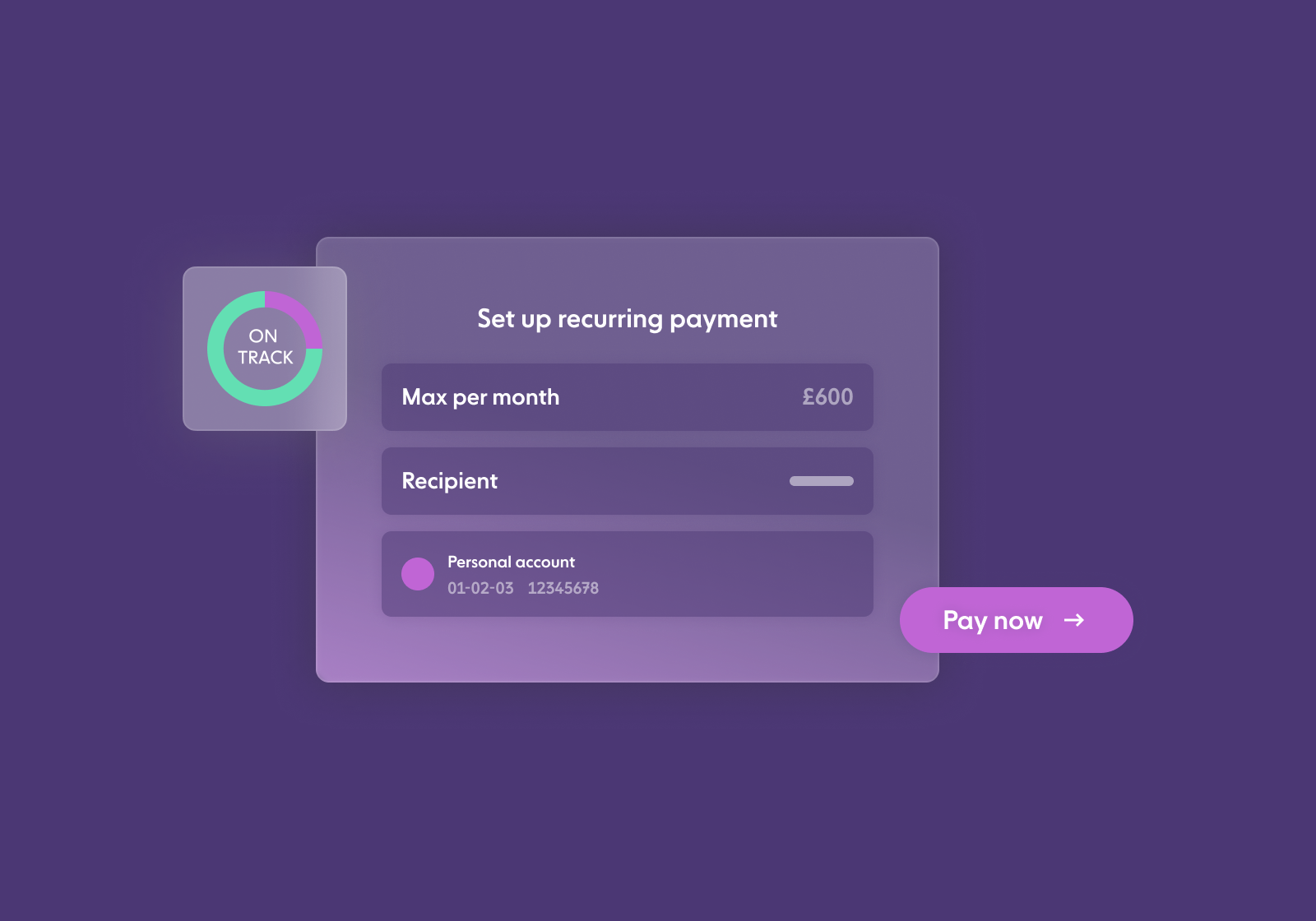

Variable Recurring Payments (VRP) are an important milestone for open banking. They have already added the ability for customers to ‘sweep’ funds from one account to another they own. This helps customers optimise their finances by moving funds where it could, for example, earn more interest or avoid overdraft fees.

The next iteration of VRPs will transform the way payments are made online. These ‘non-sweeping’ or commercial VRPs will allow customers to pay for goods and services and eclipse current traditional payment methods such as Direct Debit and Card on File. They will offer a new level of payment automation, greater transparency, and control over their finances.

5 Building trust with secure data and payments

The ability to make payments securely and with confidence is key to winning customer trust. Customers must feel secure or they will simply not complete payments or requests for data.

Open banking has enabled the development of Confirmation of Payee (CoP), and when in place it checks that funds are being sent to the legitimate and intended recipient. CoP can also reduce operational costs for businesses, improving the digital journey for customers and the overall user experience as businesses strive to maximise conversions.

Yapily and the open banking Infrastructure

The Yapily platform enables connection to an open banking API to access the most extensive coverage across the UK and Europe for both consumer and business accounts. Building with Yapily helps unlock versatile use cases across data and payments to create the best user experiences for customers.

Our ready-made user interface for single payments API, called hosted pages, makes integration and implementation swift and effortless. This white-labelled product streamlines the payment authorisation process while taking care of compliance and security obligations for you.

Risks associated with redirection to external sites are mitigated, ensuring a more secure environment for payment authorisation. This not only benefits you but also enhances the trust and security of your end-users.

Yapily will continue to lead the charge on API developments as open banking and its ever-evolving use cases continue to deliver change, driving innovation and consumer empowerment.

Speak with a Yapily open banking expert and unlock the full potential of our cutting-edge technology for your business. Contact us now for a tailored consultation and step into the future of banking!